Specialty insurance involves risk protection for unusual circumstances, which typically include very large protection requirements for certain perils that could impact an extensive list of commercial assets. In contrast to a more typical insurance arrangement in which a single carrier accepts the risk of insuring a client’s assets, large specialty insurance plans can frequently require multiple carriers to share the risk.

As an example, businesses that operate many locations in a natural disaster zone (hurricanes, tornadoes, earthquakes, or hailstorms) may need to protect hundreds of buildings from disaster risk exposure throughout a wide geographic area. A major disaster impacting a large number of locations could produce a massive claim payout that one provider could not handle.

The process of compiling details for specialty coverage and distributing those details to prospective underwriters through a large insurance marketplace is very complex. A broker must spend time with the client to learn about the business, review coverage history, and evaluate perils and risks. Whether the process is manual or electronic, there are inefficiencies and a potential for errors that negatively impact profit for all market participants.

The following is a more in-depth look at the scope of the challenges faced by brokers and underwriters in specialty insurance markets, along with potential improvements gained by intelligent document processing of slip cases. The ultimate objective for the insurance market is to handle more policy volume, without significant cost increases, which leads to profit optimization.

Overview of Specialty Insurance Process

When a business requires unusual, complex or large-scale risk protection, it can approach a specialty insurance broker who will engage with an underwriter at a specialty carrier or a specialty lead underwriter at a syndicate. A syndicate is a group of insurance underwriters that share the risk of coverage in varying amounts.

The broker compiles key details of the coverage, including perils to be covered, previous policies and claims for the company, and schedule of values (assets to be covered). These details are presented in a slip case to the lead underwriter for preparation of a quotation and negotiation on terms. The details are run through a rating engine and the coverage is priced.

The policy and quote are then submitted to the market where underwriters can follow on for a percentage of the total coverage on the same terms. For instance, Underwriter A might agree to take on 15 percent of the risk, Underwriter B 10 percent, and so on, until the entire policy is covered.

The coverage agreements are then certified to ensure there are no mistakes, and that the underwriters have a clear understanding of exactly what is covered and what risks they assume with their commitment. Mistakes do happen, which requires contract adjustments and other fixes. When everything is finalized, the policy is sent to the clearing house where it is stored for reference in the event of a claim.

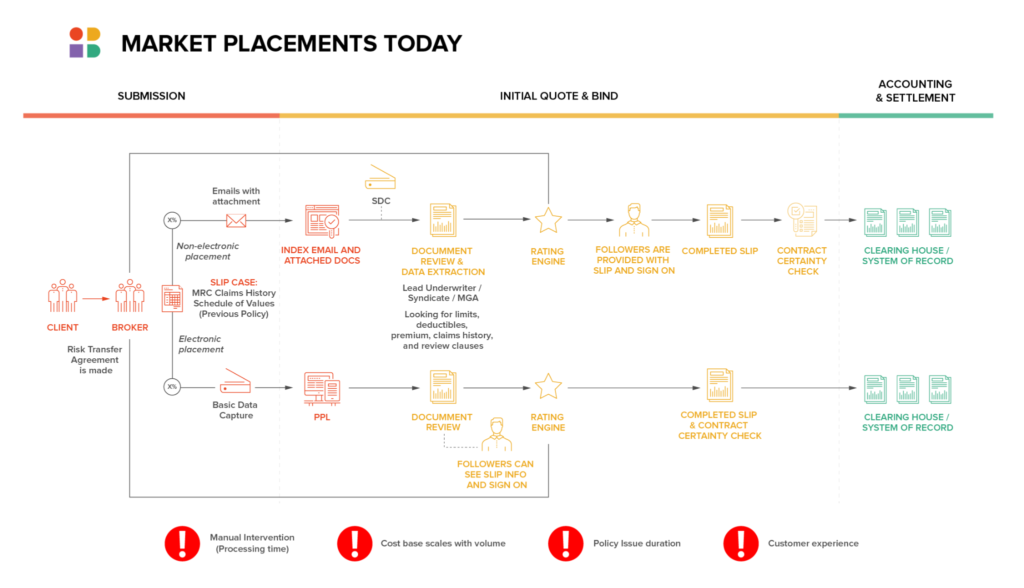

Efficiency and Accuracy Issues in Slip Cases

Slip cases are typically sent to the lead underwriter in an email with several attachments, or submitted through an electronic placement system. The coverage details are traditionally pulled manually by the lead underwriter for the purposes of running the quote on the policy and preparing the submission for the market.

The data in the email and attachments is somewhat unstructured and highly variable. The perils covered can vary greatly based on the company type, size and scope, and other factors. Because of these data variables, there are many inefficiencies in the traditional manual process. Mistakes caused by human error are costly and lead to coverage delays.

Lloyd’s of London is one of the largest markets in the world for insurance policy trading. It has historically suffered from losses due to a high expense ratio, which has averaged around 37 percent. Some underwriters make a good profit, while others don’t, but on the whole, the marketplace suffers in terms of profit due to these inefficiencies.

Intelligent Document Processing Benefits

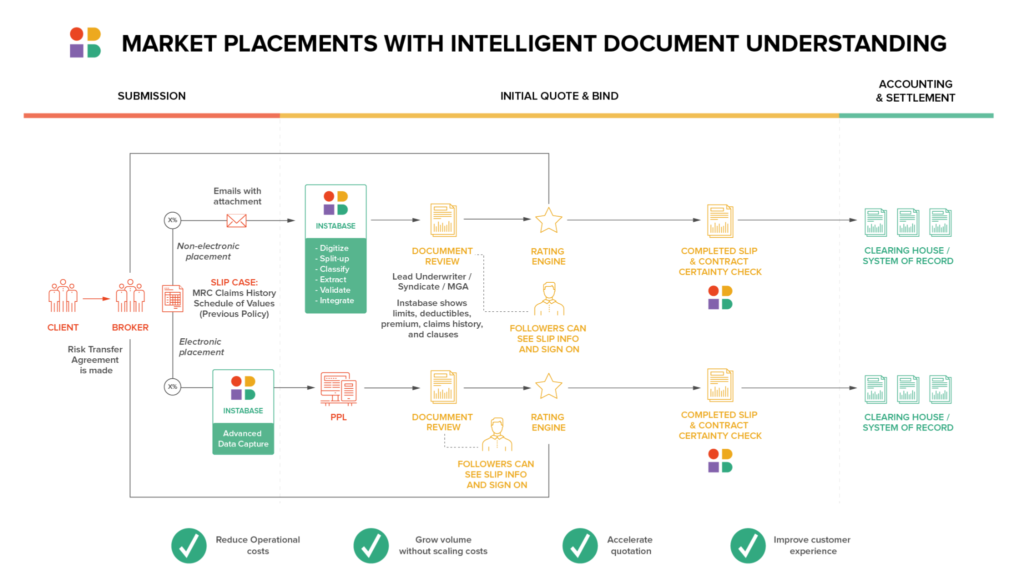

The capabilities of Instabase’s intelligent document processing addresses the inefficiencies and errors in the specialty insurance intake process perfectly. Instabase is able to index slip cases, and initially splits the email from the attachments. It then digitizes, splits, and classifies the data, and detects any missing information. In doing this, all relevant information is available in a structured and clear format for all involved underwriters and market participants. The policy is collated and eventually submitted to the clearinghouse.

There are several critical benefits achieved with The Automation Platform for Unstructured Data from Instabase, including:

- Accelerated quotations: By automating unstructured data during the specialty insurance intake stage, Instabase is able to greatly expedite the timeline from coverage request to quotation. The client knows the rate sooner and the market has time to consider its risk-protection position.

- Reduced error rates: Instabase has high accuracy rates when automating unstructured data, which means error rates are reduced and certification checks are more accurate. There are fewer rechecks and fewer delays in submitting policies to the clearinghouse.

- Reduced operational costs: By eliminating manual steps in the process, along with inefficiencies caused by errors and delay, intelligent document processing reduces costs.

- Higher placement volume without scaling costs: All of the other benefits described result in the ability of brokers and underwriters to transact a higher volume in the market without cost-scaling, which improves combined ratios and collective profit.

Let Instabase Tackle Your Specialty Insurance Challenges

The specialty insurance process is very complex. Brokers must gather and document a high volume of data on the client, perils, assets, policy history, and more. They must then organize that data and submit it to the lead underwriter for quotation. Then, multiple follower underwriters review the policy details and quote and ultimately share the risks of protection.

In the traditional manual process, the variability and unstructured nature of slip cases lead to inefficiencies and errors. These issues contribute to high expense ratios and market inefficiencies that cause lower levels of profitability among all insurance market participants.

The Automation Platform for Unstructured Data from Instabase can revolutionize large insurance markets by reducing inefficiencies and errors in the intake process. The net result is that cost efficiencies improve, errors are reduced, and insurers have much higher profit potential. Leverage Instabase to automate document processing in specialty insurance.

Leverage Instabase for speciality insurance.

Automate slip case processing with intelligent document understanding.