There are few processes that the average person goes through that are as document-reliant as mortgage origination. Loan documentation can be hundreds of pages long, with mortgage customers providing a variety of documents such as pay stubs, bank statements, and rental agreements to support their applications and lenders providing all the legal documentation necessary to complete the loan process.

For the mortgage customer, the process can be frustrating, but manual systems do a number of disservices to the involved mortgage team, too. Manual data entry slows the approval process, makes for a tedious experience for mortgage personnel and prevents departmental growth by limiting its resources.

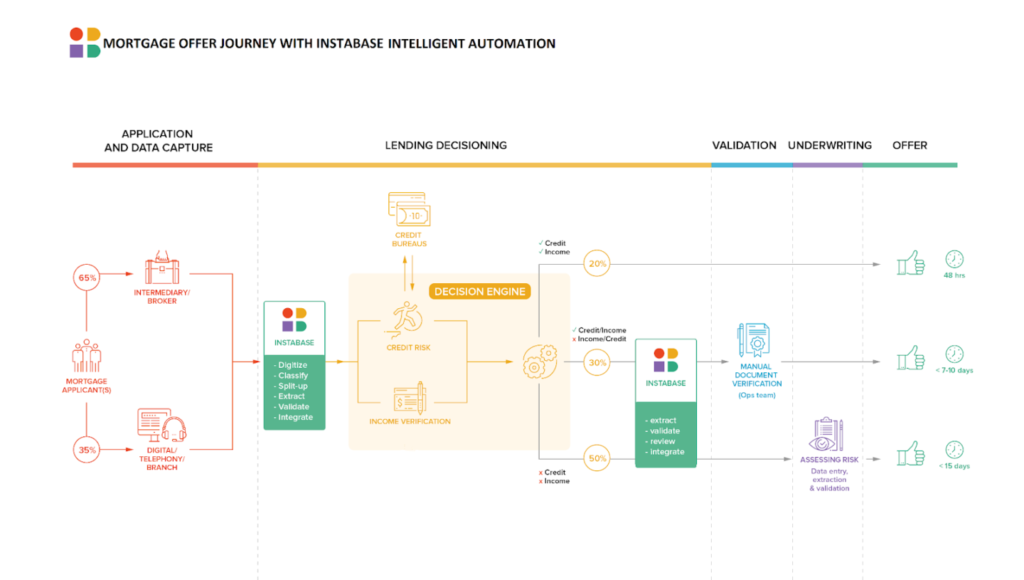

But it doesn’t have to be this way. Adding document understanding technology that digitizes, splits up, classifies, and extracts needed data to the intake process can be a game changer for a mortgage team, freeing up capital of both the human and financial variety and reducing headaches for all involved.

Here are some ways that intelligent automation can revolutionize the mortgage business.

Lowers operational costs

Those financial institutions not using a document understanding platform to automate various time-consuming, mortgage-related tasks are doing those tasks manually — and paying dearly for it. Why? Because they rely on their human employees to do these tasks. Switching to intelligent automation with a document understanding platform slashes these costs, said Tom McCann of Instabase’s financial services department.

“We enable mortgage teams to free up time for their underwriters, because their time is valuable and expensive,” McCann said. “If they’re sifting through documents trying to find … data points, they’re wasting their time” as well as money.

Instabase’s flexible solutions prepopulate systems for mortgage departments, allowing the underwriters to return to the real, brain-power-required work for which they were hired and which truly grows a business. Case in point: one large U.S. retail bank, an Instabase customer, foresees a savings over three years of nearly $5 million following implementation of Instabase technology and is now automatically processing 1.4m pages per month.

Improves mortgage customer experience

Patience may be a virtue, but few people have it, particularly when waiting for finalization of a process that will determine whether they get to own a home. And in the COVID-19 era, the perfect storm of decreased face-to-face interaction between people, heavier call volume on service-agent lines and upped customer impatience has created harder-to-please consumers. That’s problematic for an industry that relies heavily on referrals for its business.

“It’s been a complicated year for the mortgage industry,” Jim Houston, managing director for consumer lending and automotive finance intelligence with J.D. Power, told Realtor magazine in late 2020. “Between surging customer volumes on the origination side, an influx of customer inquiries on the servicing side, and a workforce that has been completely displaced by the pandemic, resources have been stretched to their limits. That strain is showing up in slower loan processing times, missed opportunities to communicate, and unreliable self-service tools.”

The financial institution that manages to overcome these obstacles is far more likely to not only remain viable, but to thrive, in large part because its customers are happy. Reduced wait times, quicker responses to queries, less back-and-forth between borrower and mortgage team and other increased efficiencies made possible by intelligent automation make for a better customer experience. And a happy customer makes for many referrals.

Frees up company resources for business expansion

Financial institution employees spend untold numbers of hours each year manually reviewing mortgage documents, filling in digital data fields and splitting up, classifying and transcribing multi-hundred-page loan packets. Already mind-numbing and time-consuming, this process might be somewhat more manageable were it not for the fact that crucial incoming documents arrive in a vast array of incompatible formats. Tally all these factors and the resulting figure is a sum of money far greater than what most banks probably realize they are wasting each year. Then add in that with so many resources devoted to manual processes, there’s probably little time for business expansion, and you get a stagnated business.

Instabase technology is “enabling mortgage lenders to be able to grow,” Toby Burton, Business Value Consultant with Instabase, said. “We can understand the complex documents that are coming in, and we can provide our customers with a platform that’s really easy to use, with these building blocks that they can string together to first digitize everything that’s coming in — so it’s in consistent digital format — to then speed up processing the packets of documents … and then classify each thing.”

The intelligent platform can differentiate between types of documents (such as bank statements from pay stubs), saving employees from having to do the sorting, Burton said.

Without such a solution, a financial institution faces a choice between two moves with equally unpalatable results: Hire more people (a significant expense) or continue to take up the valuable time of existing employees. Both options mean lost revenue.

Using document understanding software instead lets a business “do more work without having to hire more people,” McCann said. “It’s a scalable solution.”

Is your organization ready for a solution that will delight mortgage customers, free up employees for the work they truly enjoy, and allow your mortgage business to finally grow? Build better mortgage customer experiences at scale with Instabase today.

Build it better with Instabase

Provide better mortgage customer experiences at scale.