Improve Operational Capacity and Risk Visibility in Commercial Lending

Time to cash delays due to constraints on operational capacity and risk visibility are constantly on the minds of commercial business leaders. Whether it is resistance to change or obstacles impeding innovation, a lack of digital automation is a challenge to optimization of either of these areas. However, government pressure for small-business loans and market expectations for timely processing mean that lenders have no choice but to find the right solution to overcome these challenges.

Intelligent document processing is the primary lever to simultaneously and cost efficiently reduce time-to-cash, increase operational capacity and achieve more reliable risk visibility.

Overview

Following COVID, government and regulatory bodies have been pushing commercial lenders to expand their loan capacity to accommodate more of the capital needs of small and medium-sized companies. However, many lenders do not have the operational capacity to process loans efficiently. Additionally, efforts to rush application processes create concerns with accuracy in risk assessment.

Despite a major digital transformation across the financial services sector following COVID, unstructured data still poses an ongoing challenge. Commercial underwriters need several complex documents and data to complete their review processes. Traditional document understanding systems are fairly good at processing structured data from standard application forms, but are less equipped to process unstructured data. The problem is that much of the documentation coming into commercial lenders falls into the unstructured category.

To underwrite a higher volume of loans while maintaining effective risk-assessment practices, lenders need a better system to speed up the underwriting process and eliminate inefficiency.

Core Challenges

Through their digital transformation journeys, commercial lenders have integrated cloud-based solutions for customer relationship management, origination system workflows, and many other business functions and processes. These systems rely on structured data that is neatly organized, allowing for further business decisioning and conventional analytics reporting. However, most of the data used in the underwriting process comes into the business in unstructured formats.

For example, underwriters need identification documents, articles of incorporation, financial statements, collateral valuations, proof of insurance and other documents. These documents are typically received by the lender as email attachments or via the postal service. They contain variable, unstructured data that cannot be used as-is by other technology systems.

At the point of application, underwriters spend a lot of time in going back-and-forth with applicants to verify information, identify gaps, or to request additional documentation. This laborious work is inefficient and takes underwriters away from their key role in the underwriting process.

Once all the requisite information is received, qualified underwriters spend a further chunk of valuable time in reading and reviewing documents and keying in basic data in several different systems manually. This process is tedious, requires many man-hours, and increases inaccuracies in loan reviews and risk assessment. Manual gathering and organizing of unstructured data leads to incomplete, inaccurate, or missing data – further leading to an incorrect estimation of the risk in a loan.

A major factor in risk assessment is a review of collateral valuations. These valuations are usually submitted as PDF documents through email or shared folders. Values of collateral change over time, and borrowers can also change the collateral backing a particular loan. Inability to have clear visibility of all the data associated with collateral can dramatically affect the risk profile of a loan portfolio.

When considered at an aggregate level, inaccurate estimates of risk and collateral position can have a huge impact on the capital reserves a lender has to set aside – thus impacting their overall cost of capital – with implications of much higher magnitude reaching far beyond the lending business.

The Solution

Clearly, the inability of commercial lenders to handle unstructured data is one of the largest hurdles to scaling their businesses and managing risk. At present, most rely on manual processes to deal with unstructured data that doesn’t fit neatly into their digital systems. However, this approach slows down the underwriting process and presents numerous chances for risk-assessment errors.

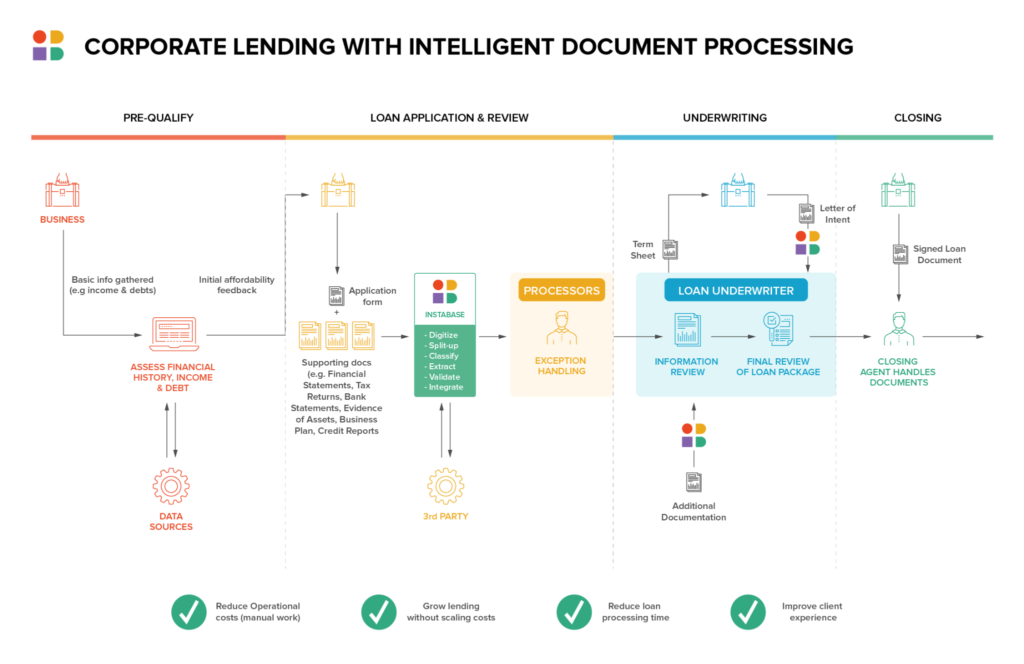

Intelligent document processing is the most powerful lever for commercial lenders to address these core challenges. Instabase’s automation platform for unstructured data is built to handle unstructured data found in highly variable, complex documents. Instabase’s technology has proven effective across a variety of industries burdened by a large volume of highly variable documents.

At the point of ingestion, Instabase can automatically split up a document packet, classify into different document types, and instantly identify any missing or invalid documents. This can trigger immediate notifications to customers, saving time in to-and-fro, giving customers visibility, and freeing up relationship manager time. Instabase can then automatically extract the requisite data points, validate these with internal and external systems, and feed into downstream pricing and decisioning systems which can then be used by underwriters to make go-no go decisions.

The following benefits are achieved with intelligent document processing:

- Manual processes are eliminated or reduced, which frees up underwriters to focus on loan reviews and risk assessment.

- Lenders can operate with a more lean workforce due to the time saved from elimination of tedious manual processes.

- Unstructured data is no longer missing or inaccurate, which improves efficiency and risk visibility.

- Lenders can cost-efficiently scale the business by improving operational capacity due to better resource efficiency and a more accurate view of capital requirements.

- The customer experience is dramatically improved due to faster application time periods and improved process communication.

The Future of Commercial Lending

Commercial lenders are under intense pressure from a variety of sources. The government and regulatory bodies are pressing hard for lenders to provide more capital to small businesses. However, at the same time, lenders face heightened requirements for regulatory compliance and reporting standards.

The market is another source of pressure. Business operators are in great need of working capital to sustain and grow their businesses following the pandemic. They don’t have time to wait for slow application and underwriting processes. If a lender is not able to provide approval and funding in a reasonable amount of time, prospective borrowers will simply seek out other options.

Despite this pressure to improve operational capacity and deliver funds in a timely manner, lenders must stay disciplined with risk assessment. Intelligent document processing is the only practical way that commercial lenders can compete in the current climate of the financial sector.

By automating unstructured data with Instabase, lenders gain system efficiencies and improve accuracy in extracting unstructured data. Underwriters are equipped with the organized documents and data they need to review applications with awareness of collateral valuations and other risk factors. Timely decisions are provided to applicants, resulting in an optimized customer experience.

Further Reading

%20(2).png)

.png)

.png)